May 2026 | Aspira Wealth, Victoria, BC Special Market Dispatch – The Wall

Chris Raper, CIM, CFP ®

As I write on Tuesday, May 12, 2026, I am deeply convinced that the world is about to hit a severe energy shortage, one that I have dubbed The Wall. I see it as inevitable and present the evidence below. What I can’t tell you is how much it is going to hurt. What I can tell you is where we are invested in and why. One of the reasons I write these missives is because it helps me clarify my thinking and hopefully make better investment decisions.

Here goes – the feared energy shortage as a result of the closing of the Strait of Hormuz is showing up in real time:

- Europe’s jet fuel inventories at key hubs like Amsterdam-Rotterdam-Antwerp have already plunged 50% since the conflict began and their natural gas inventory levels are currently at roughly 35%, the lowest since 2018 – historically, they should be at 47%.

- Meanwhile, Southeast Asia is facing a severe energy supply crisis. The region, which relies on the Middle East for roughly 85% of its oil imports, is experiencing "energy triage" and panic buying is becoming the norm. The Philippines, Thailand, and Vietnam, have all gone remote/reduced work weeks and reduced travel to cope.

- Last Sunday night, India’s PM Modi was on national television, asking citizens to stop buying gold, avoid foreign travel and to cut fuel consumption to save foreign exchange by any means necessary. Think about that – roughly 18% of the world’s population facing a lockdown-style blow to their economy – one where the PM has to beg its citizens to help with the crisis.

How much oil production has been lost? As of last week, the world has already lost roughly 700 million barrels of production. That is the equivalent of grounding every plane in the world for the next 90 days. Furthermore, I am of the belief that this conflict is not going to be resolved anytime soon and even if it gets resolved tomorrow, it will take months to restore production and, more importantly, years to restore confidence in the region. In the interim, the world will fight last year’s war by diversifying suppliers just as it did after the 1973 embargo. Yes, I am old enough to remember that 😊. That bodes well for Canada and our domestic energy producers.

If the thought occurs to you, how can the U.S. stock market be hitting all-time highs when it seems like the world is going into an energy-deficient lockdown, the likes of which we have never seen since the 1970s, I too wonder the same and thus, our cautionary stance.

To me, it seems like the world is trading AI chess pawns on extreme optimism while there is far too little focus on The Wall. We have seen exuberance with the hyper-scalers (GOOGL, AMZN, MSFT, META) and, over the last few weeks, it feels like we just moved over to the semiconductor space, and we might be setting up for a blow off top this week.

To be clear, I think there are going to be some great investment opportunities in the adopters of AI. I am less convinced with the creators of AI, and admittedly, I find it harder to grasp what will be.

The above said, there is one common thread that could/will slow down the growth of the entire AI industry – it is energy; specifically, electricity.

What does one need to produce copious amounts of new reliable electricity – energy in other forms. That’s why we own Cameco across all of our equity strategies, one of the world’s largest global suppliers of uranium, and 49% owner of Westinghouse Electric Company, a company that was just pledged $80B by the U.S. government to build new nuclear reactors.

Likewise, we own various natural gas producers because we understand that nuclear can’t do it alone. You also need a lot of copper where future supplies are far from certain and the situation is further aggravated by the fact that ~50% of the world’s seaborne sulfur passes through Hormuz. You need sulfuric acid to refine copper. We are grateful for our investments in Lundin Mining and Exchange Traded Funds (ETFs) COPX and PICK.

Sticking with Hormuz, at least 25% of the world’s fertilizer passes through there as well. The results have been predictable. To wit, the new 52-week high on wheat and our ownership of Canada’s flagship fertilizer producer, Nutrien.

Chart courtesy of StockCharts.com

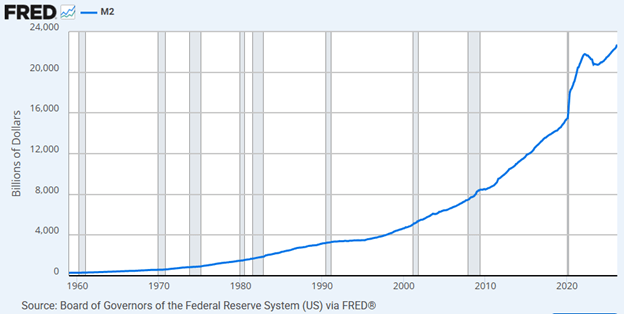

Meanwhile the world’s global money supply (fiat currency) only grows, bolstering our case for higher inflation, higher long-term interest rates and our continued interest in the gold complex.

United States, like most of the world, has had a significant increase in their money supply since 2020.

The expected inflation rate in U.S. is now reaching its highest levels since 2022:

The 10-year treasury yield is now moving towards its highest level in the last 12 months:

Chart courtesy of StockCharts.com

Summary & Conclusions

Notwithstanding the significant returns we have had year to date, caution is warranted. Yes, the Strait of Hormuz could open tomorrow and even if it does, the impact will be felt over months and years, not days and months. If the closure continues for months ahead, a global recession is certainly plausible. The good news is that Canada and the U.S. are in an enviable position, relative to the rest of the world. Yes, AI is exciting and I use it every day. Investment-wise, I am biased to the second and third derivative enablers (copper/electricity) and the adopters of AI, as opposed to the creators.

Finally, it is important to note that Alex and I don’t always see the world the same way. That’s a good thing. It helps us make better decisions. In that spirit, the postscript is Alex’s response.

Postscript by Alex Vozian, CFA

Chris lays out a thoughtful case for a potential energy shortage, and many of the underlying observations are valid. Where I would differ is the degree of inevitability.

One key difference versus past crises is that the global economy is more adaptive today. The share of oil in total energy consumption has declined over time, and supply chains are generally more flexible than in prior decades.

Several developments could reduce the severity of any disruption:

- Middle Eastern supply can be partially redirected via pipelines and alternative routes

- Demand typically declines when prices rise

- Release of strategic reserves and potential reduction in sanctions on Russian supply could help the supply

From a market perspective, it is also important to remember that markets are forward-looking. We may already be observing one of the worst scenarios for global energy supply, with simultaneous tensions and damaged infrastructure in the Middle East and Eastern Europe. If that is the case, I would expect the situation to get less bad. Markets do not require a return to “normal” to respond positively; often, “less bad” is sufficient to support improvement (i.e., less expensive oil prices for end consumers).

In practice, we acknowledge various scenarios. We see value in selected energy and materials exposures, while recognizing that global systems tend to adjust, and outcomes rarely follow a single path. Undoubtedly, at some point in the future, we will find attractive opportunities in the technology sector, again.

Written by: Chris Raper, CIM, CFP®

Co-Founder | Wealth Advisor | Cross Border Specialist

Aspira Wealth of Raymond James Ltd.

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd./Raymond James (USA) Ltd is not responsible for the availability or content of these external sites, nor does Raymond James Ltd/Raymond James (USA) Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd/Raymond James (USA) Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()