THE QUARTERLY COMPASS Q1 2026 | Aspira Wealth, Victoria, BC

Market context, portfolio positioning, and investment outlook from your wealth advisory team

Alex Vozian, CFA | Co-Founder and Portfolio Manager of Aspira Wealth.

Working Into Headwinds - Photo by Alex Vozian. Victoria, BC.

Quarterly Summary

- The first quarter of 2026 was particularly challenging, due to renewed confusion around U.S. trade policy, escalation of conflict in Middle East, and private credit crisis on top. Equity markets proved more resilient than sentiment alone would suggest.

- Aspira portfolios were helped by diversified positioning, including lower relative exposure to U.S. equities, higher allocation to commodity producers, and selective exposure in other sectors. While short-term outcomes are never the focus of our investment process, portfolio construction emphasised resilience during periods of stress.

- Several market sentiment indicators reached pessimistic extremes in March 2026, a pattern that historically has been more consistent with improving forward return conditions than with sustained market deterioration. Our portfolios stay near fully invested, with some minor changes expected in the coming months.

Canadian and U.S. Markets in Q1 2026

Entering 2026, corporate and investor decision‑making was already under pressure from persistent tariff uncertainty, elevated costs, and slowing real income growth. These conditions contributed to more cautious hiring, capital investment, and discretionary spending across several sectors.

In March, this fragile backdrop was further disrupted by renewed conflict in the Middle East, which briefly pushed energy and transportation costs higher and added to near‑term inflation concerns. Rather than a single dominant shock, the quarter was defined by multiple overlapping uncertainties, complicating forecasting and risk‑taking.

Measures of consumer confidence reflected this strain. By early spring, sentiment indicators had fallen to levels typically associated with economic stress, driven by higher fuel prices and heightened geopolitical risk. In fact, the University of Michigan Consumer Sentiment Index fell in April 2026 to its lowest level since the survey began in 1952. Historically, low consumer confidence levels were often followed by positive stock market returns.

Equity markets, however, proved more resilient than sentiment data alone would suggest. Canadian and U.S. indices both experienced sharp 10% drawdowns during the March selloff, while recovering at the first signs of de-escalation in Middle East. Once again, we were reminded that having a long-term focus is better to reacting than daily news.

Canadian (XIC.TO - red line) and U.S. (SPY – blue line) stock markets since start of 2026

Chart courtesy of StockCharts.com

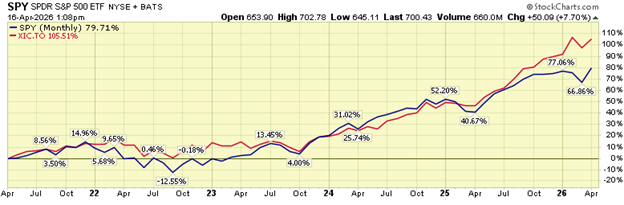

Five Years of Resilience and Growth

Despite trade disputes, military conflicts, banking crisis, private credit fears, and a global pandemic, disciplined equity investors have experienced strong cumulative returns over the past five years. This period serves as a reminder that markets have historically adapted to repeated economic and geopolitical disruptions, even when short‑term volatility was significant.

At the same time, the strength of recent returns reinforces the importance of realistic expectations looking forward. Elevated starting valuations suggest that future returns might be more moderate than those experienced over the earlier cycle, even as long-term investment opportunities stay intact.

Canadian (XIC - red line) and U.S. (SPY – blue line) stock markets – 5-year chart

Chart courtesy of StockCharts.com

Positive Signals from Leading Indicators

Several leading economic indicators we monitor closely provided constructive signals during the quarter.

Copper prices remained near record levels throughout Q1 2026, repeatedly trading above $6 per pound. This strength aligns with our longer standing view that copper demand increasingly reflects investment in data centres, electrification, and energy infrastructure, rather than solely traditional industrial activity. Limited new supply and long project lead times continue to underpin the medium-term outlook. Currently, all the Aspira equity strategies participate in this theme through selective exposure to copper miners.

Semiconductor equities also demonstrated notable resilience. The Semiconductor ETF (SOXX) rose significantly year-to-date, reflecting sustained demand for advanced computing, data infrastructure, and automation. While volatility stays elevated, the longer-term investment case for semiconductor capacity expansion continues to be supported by structural demand rather than cyclical excess.

Investor Fear peaked in March 2026 (a.k.a.“opportunity”)

Investor fear reached elevated levels in last few weeks - measures of market volatility and sentiment both signalled material stress:

- Volatility index (VIX), a market fear indicator, just reached highest level since tariffs’ panic of April 2025.

- CNN’s Fear and Greed Index - recorded an extreme level of fear in the last weeks of March.

Taken together, these signals suggest that investors had largely exhausted their fear, with markets responding less and less to new bad news.

Additional stock market gains are never guaranteed, but we are significantly more optimistic today compared to three months ago, because of how markets discounted worst case scenarios in March.

Our Investment Outlook and Strategy

We expect equity market returns over the next five to ten years to remain positive, though more moderate than those achieved over the past five. Our current positioning reflects this assessment.

Portfolio Positioning

- All equity strategies to stay near fully invested, reflecting our confidence in equities as long‑term wealth‑building assets.

- Continue to focus on dividend-paying stocks for income and stability.

- Maintain diversified exposure to high-quality equities in both Canada, and the U.S.

- Maintain our small & selective exposure outside North America.

- Keep or trim slightly, our current exposure to gold, silver, copper, energy, and uranium – we see some of the tailwinds losing momentum.

- Keep or increase our current exposure to technology sector – we see some opportunities after major 2026 selloff.

- Maintain a neutral stance on USD vs. CAD currencies.

Risk Management

- We see a lower probability of a correction larger than 10% in the short/medium term.

- We plan to deploy some of the available cash across new and existing accounts over the coming months, while maintaining diversification at both the position and sector level.

Monitoring the Landscape

- Closely watch the upcoming corporate earnings season for signs of strength or weakness across sectors.

- Continue to watch trade, fiscal, monetary, technology, and geopolitical developments – without over-reacting.

Thank you for your continued trust.

Alex Vozian, CFA

Co-Founder and Portfolio Manager

Aspira Wealth

Thursday April 16, 2026.

![]()