INVESTMENT MARATHON #10 • January 2023

The building blocks of Aspira Wealth’s long-term investment strategy

Newsletter by Alex Vozian, CFA, Co-Founder and Associate Portfolio Manager

Subscribe to our newsletters in one click.

Dozens of peacocks qualified for an early-bird special at the Beacon Hill Park Theatre, Victoria, BC.

SUMMARY

- Canadian and U.S. markets update

- Performance update

- ATS Corporation (ATS . TO) – one of our holdings

- Dream job!

- How we help

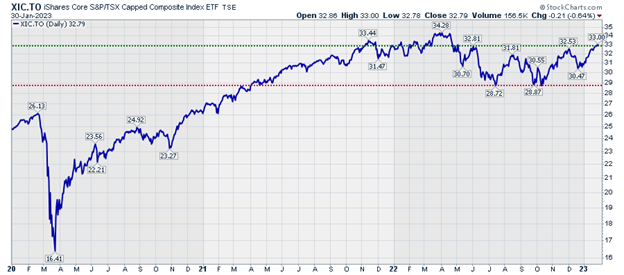

CANADIAN AND U.S. MARKETS UPDATE (2023-01-30)

Both Canadian and U.S. equity markets are showing signs of strength in early 2023 - now trading at a 5-9 month record highs level, after being volatile during most of 2022 (see charts below).

The news is filled with headlines about possible recession this year, about tens of thousands of jobs being lost (mostly in the tech sector), as well as about various companies lowering their earnings expectations. While challenging to employees and business leaders, this environment is ok for investors:

- The stock market usually bottoms several months before the end of the recession.

- This particular recession (if we are in one) is the desired outcome of central banks, who aggressively raised the interest rates in order to fight inflation. The weaker economy is expected to slow down the inflation level. The decline in inflation will allow central banks to gradually lower interest rates that in turn will help asset prices.

In summary, our list of reasons for long-term investors to remain optimistic is largely unchanged since our November 2022 publication.

✓ Negative Sentiment – less extreme than last time, but sentiment is negative enough to be considered as attractive from contrarian perspectives. This was illustrated when I attended the largest economic forecast conference last Thursday; the guests from Canada, the United States, and the U.K. were all worried about the timing, depth, and duration of the economic downturn.

✓ Slowing Inflation – continued signs for slowing down.

✓ China Trade Shutdown - China is quickly reopening.

✓ European Energy crisis - European Natural Gas benchmark prices continue to collapse – now more than 70% below 2022 peak.

✓ Favorable Seasonality - Stock markets (at least in the U.S.) tend to do better from Nov to April (compared to rest of the year), as well as immediately after US midterm elections.

✓ Long Term Focus & Discipline – Equity markets tend to offer superior long term returns and more so when investing in diversified portfolios of high quality businesses. It is impossible to determine where the market will be in the short term, but we expect it to be higher in the long run.

Charts courtesy of StockCharts.com

PERFORMANCE UPDATE (2023-01-30)

Most of our in-house investment strategies ended the year 2022 with better results than the market average. Chris shared details in his recent publication Where We Landed For 2022.

For January 2023, our primary investment strategy, The Dividend Value Discipline™, is up about 3.5%, modestly lagging market averages.

While we are pleased with our results for 2021 and 2022, we place no weight on short-term results, good or bad, and neither should you. In fact, we occasionally make decisions that negatively impact short-term performance if we think we can improve our long-term returns and/or lower risk levels.

A HOLDING WE OWN – ATS Corporation

ATS Corporation (ATS . TO) is a company that we expect to prosper as the world struggles with labor shortages while the global economy is in “de-globalization” mode (multiple Western countries are trying to rely less on their former suppliers from Asia and Eastern Europe).

ATS is a Canadian company providing automation solutions through custom automation, repeat automation, automation products and value-added services, including pre-automation and after-sales services. ATS serves multinational customers in markets such as life sciences, food & beverage, transportation, consumer products, and energy. Founded in 1978, ATS employs over 6,000 people at 50 manufacturing facilities and over 75 offices in North America, Europe, Southeast Asia, and China.

After following its progress over the course of several years, we began adding ATS to our core investment strategy - The Dividend Value Discipline™ - in late 2022.

Our internal estimates of quality and investment return are attractive for ATS. We were attracted by strong management, economic moat, and industry tailwinds:

- Great results under the new management team - introduced a new 'ABM' corporate strategy in 2017 and achieved great results: successful strategic acquisitions and performance improvements.

- Solid competitive advantage - large scale, significant switching costs for customers, strong research and development base. The wide economic moat is confirmed by improving return on invested capital.

- Significant industry tailwinds. Exposure to accelerating markets. De-globalization and labor shortages are a great tailwind for automation solutions. During the past 10 years, the growth in industrial equipment spending around the world was suppressed by the aftermath of the financial crisis of 2007–2008, slowing Chinese economy, oil crash of 2014, environmental stewardship, and other factors. We expect the future 5-10 years to be quite the opposite (i.e. very favorable).

- Improving environmental, social and governance (ESG) score. Due to relatively small company size, ATS is not covered by most major ESG ranking providers. The only score available to us (from Sustainalytics) ranks ATS worse than average. That assessment was completed in September 2022 – i.e. before ATS latest Sustainability Report from December 2022 (where ATS reported progress towards most of its ESG goals.). We assume the ESG score of ATS to improve in the near future.

- Dividend status. On very special occasions we research and buy companies that are not yet paying dividends. ATS is one example. The lack of dividend is not surprising, as smaller industrial companies operated in a relatively tough environment – the Great Recession of 2008, followed by underinvestment in the space, industrial mini-recession, trade-wars, etc. The lack of dividend payment is compensated by strength in other quality score factors, and we expect ATS to eventually initiate dividend payments.

DREAM JOB

Twenty-seven years ago, a professor told me about a remarkable job in a faraway land (referring to North America). The dream job involved just watching TV & reading the news all day to occasionally share important news with your team or clients.

In an extraordinary bit of serendipity, I ended up moving to those faraway lands with my family, and having exactly that dream job – yes, spending most of my time on following the news from hundreds of sources and trying to determine what is important.

How little I knew back then about exponential growth in volume of the information available to investors, as well as about the challenges in extracting the most valuable pieces of information (before other market participants do!).

HOW WE HELP OUR CLIENTS

An important part of how we help relates to my dream job story; we are constantly on the lookout for favourable and unfavourable developments involving individual investments from your portfolios, the overall stock market, as well as the changes in law and taxation that might affect investments in the long run. We conduct all this work behind the scenes, so you can focus on other things.

PLEASE REACH OUT

It is our mission to help our clients live out their greatest aspirations!

Feel free to reach out to discuss what is on your mind and the puzzles you are trying to solve.

- Schedule a meeting with Chris or Alex, or

- Send your questions by email to Chris or Alex.

Learn more about us by checking out our team’s page and the founders’ video.

THANK YOU FOR READING MY NEWSLETTER

Subscribe to our newsletters with one click.

Our previous publications are available here https://www.aspirawealth.com/insights.

Yes, it snows in Victoria, too! The largest snowfall since our last newsletter.

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()