Dear reader,

I hope you will enjoy the first edition of THE QUARTERLY COMPASS!

This new publication is replacing the old THE QUARTERLY OPPORTUNITY UPDATE that was written and recorded on audio by Chris Raper for over 20 years. This reallocation of resources will allow Chris time to launch our first podcast, FROM GENERATION TO GENERATION – a dad-daughter podcast focused on passing all forms of wealth to the next generation. You can read more about this here.

- THE QUARTERLY COMPASS (launched by Alex today!) - will be enjoyed most by readers who are passionate about understanding investment strategy at a deeper level.

- INVESTMENT MARATHON (launched by Alex in 2021) - will continue to be enjoyed by a broader audience, as it will cover investment-related content in a more simple and fun way.

On a separate note, I want to express my gratitude to all our clients and to my team, for all the trust and support, as I celebrate my 10th anniversary with Aspira Wealth and its predecessor, as well as celebrate 20 years in investment management and research in the North American equity market.

Alex Vozian, CFA

Co-Founder and Associate Portfolio Manager

Aspira Wealth

-----------

The Quarterly Compass - Aspira Wealth - June 30, 2023

WORRY JOURNAL - top worries of market participants and business leaders in 2023

- Inflation (in the news in 2021-2023) - inflicted by unprecedented government aid, relief, and economic security payments to individuals and corporations, relative to the amount of products and services that the pandemic-constrained economy was able to provide.

- We expect inflation to continue to decline, as supply chains are recovering from a once-in-a-lifetime shock (pandemic), supported by the tightening monetary policy (central banks increasing interest rates).

- Economic slowdown/recession (in the news 2022-2023) - on assumption that central banks will not be able to quickly fix the inflation problem and/or might increase the interest rates too much.

- We assume that central banks are near the end of the monetary tightening cycle. Even if they tighten too much, it might not matter in the long term.

- Higher interest rates and headlines about possible recession led to a slowdown in consumer and business spending (especially discretionary spending), but it seems that the economy is quite resilient. While interest rates are now the highest they have been in 10 years, they are still lower than levels seen in the previous 30 years.

- Trying to predict the timing of recessions typically doesn’t end well for most investors, so we chose to focus on the longer term.

- Even if a recession starts tomorrow, we think the downside is limited in the equity market, as typically the bottom of the stock market is usually 6-12 months before the official end of a recession. Equity market is a forward-looking animal, i.e., reflecting the near-term future expectations as opposed to where the economy currently is.

- Debt ceiling debate/potential of a U.S. default (April-June 2023) - a recurring worry in the U.S., where the negotiations often extend into the eleventh hour before an agreement is reached.

- The crisis was temporarily fixed in June 2023, i.e. discussions delayed to early 2025.

- War in Ukraine (2022-2023) - has taken a terrible human toll and seems to have no end in sight.

- While it is painful for people from the region and from around the world, we see that world trade and economy are gradually adapting to it, as it did in previous wars. Europe’s economy continues to grow and the regional energy crisis seems to have been avoided.

- Supply chain disruption (2020-2023) caused by the pandemic.

- There are pockets of concerns related to supply chains (originating from the pandemic and/or recent escalation of U.S.-China trade war), but we think that the current shape of supply chains is significantly better than it was a couple of years ago.

- Labour shortages, attracting and retaining talent (2020-2023).

- The recent pandemic induced a major shock to the labour market. We believe the labour shortage is gradually getting resolved – hiring in the technology sector is now more rational, borders are being reopened to immigration, people are more willing and able to re-enter the labour force compared to a couple of years ago. On top of this, automation and AI are likely to continue to boost productivity.

PLAYBOOK OF OPPORTUNITIES – how we seize the current opportunities

Broad equity market level: we intend to remain fully invested in North American equities.

- The much-discussed recession might be shallow, or already priced in, or even may not happen at all.

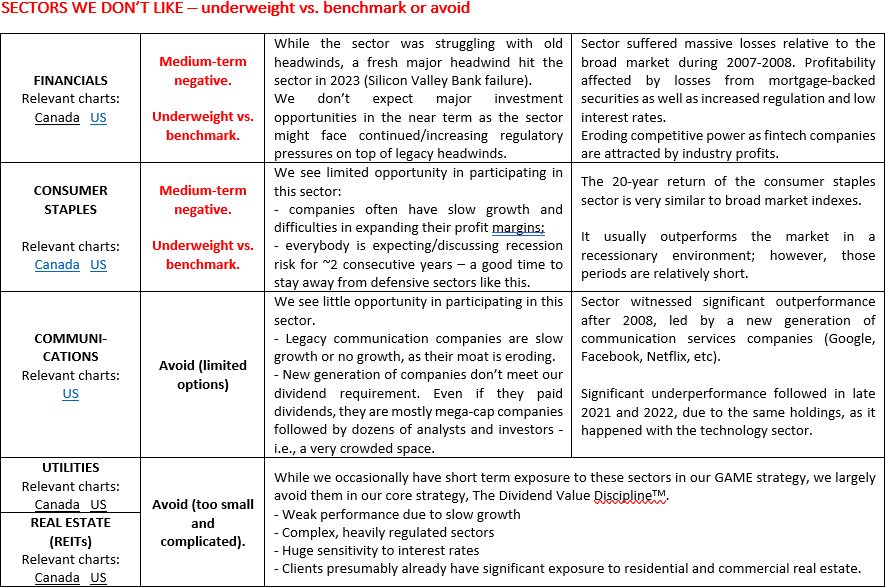

Economic sector level – we intend to stay overweight in cyclical sectors, underweight in defensive.

- Over-weight cyclical sectors – technology, industrials, materials, consumer discretionary

- Equal-weight in energy and healthcare

- Under-weight most defensive sectors – utilities, consumer staples, REITs

- Under-weight financials

More details on the sectors are available below in the section, Sector Positioning for Dividend Value Discipline TM.

BROAD MARKET OBSERVATIONS

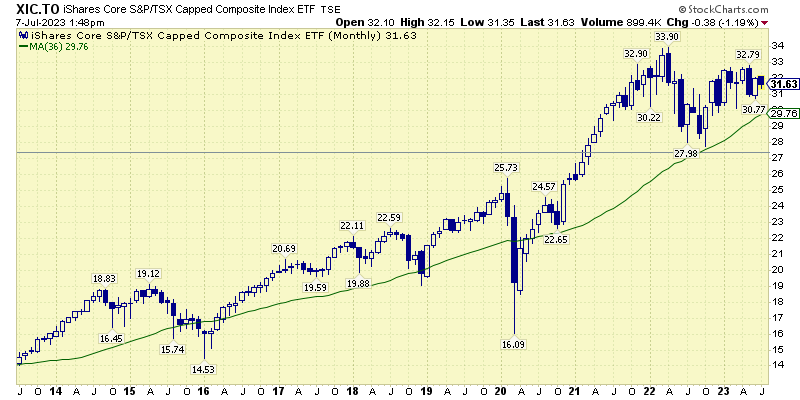

CANADIAN STOCK MARKET

- The Canadian market remains in a solid long-term uptrend, above the three-year average (green line), as it did most of the past 10 years.

- It was below the three-year average briefly, in early 2020 (Covid) and second half of 2015 (Weakness in Energy). Unlike the U.S. market, it managed to stay above the three-year line in 2023.

- During most of 2022 and six months of 2023, it remained stuck in the range of 0-20 per cent, below the early 2022 peak (grey line).

Chart courtesy of StockCharts.com

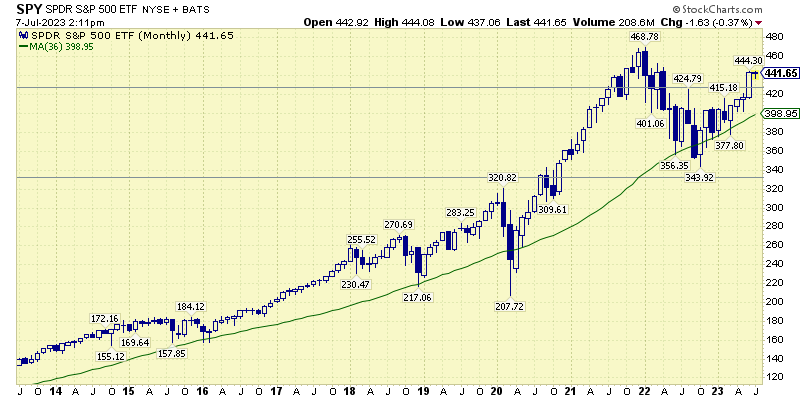

U.S. STOCK MARKET

- The U.S. market remains in a solid long-term uptrend - above the three-year average (green line), as it did most of the past 10 years.

- It was below the three-year average briefly, in early 2020 (Covid) and in late 2022 (fears of recession from higher interest rates).

- During most of 2022 and six months of 2023, it remained stuck in the range of 10-30 per cent below the 2021 peak (two grey lines).

- In June 2023, it finally broke into the range of 0-10 per cent below the 2021 peak (above upper grey line).

Chart courtesy of StockCharts.com

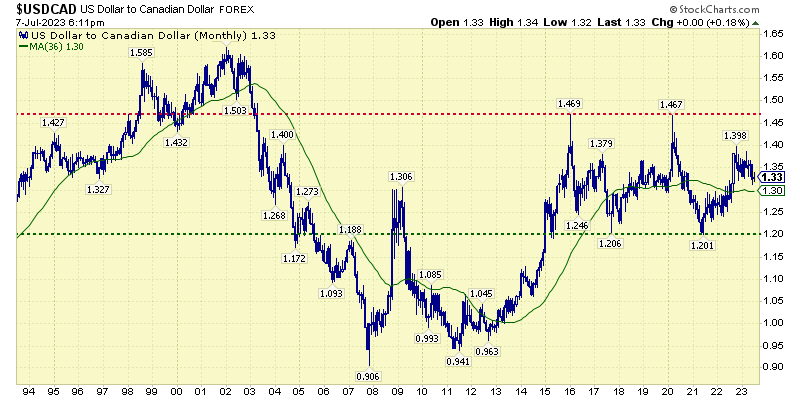

USD CAD Exchange Rate

- Over the past 30 years, the Canadian/U.S. dollar exchange rate was quite volatile, but it spent half of the time within the 1.20-1.50 CAD/USD range, including the last 8+ years.

- We assume that, over the long run, the exchange rate between CAD and USD will remain rangebound, having a neutral effect for Canadian investors with exposure to stocks listed in U.S., and for the U.S. Investors with exposure to Canadian stocks. Our assumption is based on the depth of economic connection between Canada and U.S., as well as economic policy similarities.

- We will continue to allocate 50-75 per cent of exposure to U.S. stocks, to not be limited by the rather undiversified Canadian stock market.

Chart courtesy of StockCharts.com

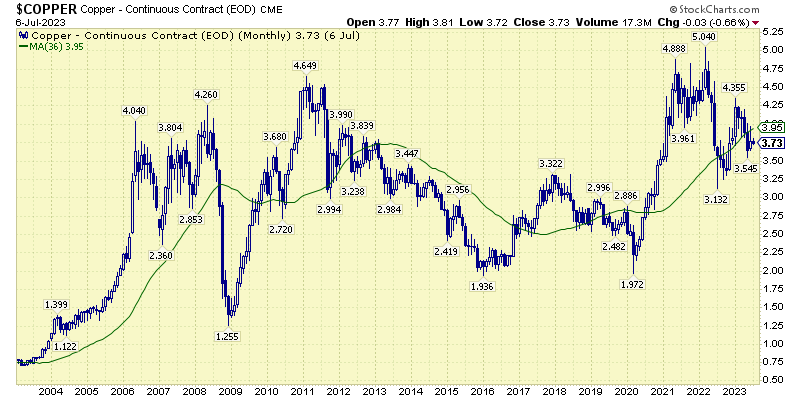

Dr. Copper

Copper price is assumed to predict turning points in the global economy, since it is used widely in most economic sectors.

- Copper price remains very volatile since mid-2022 and is down so far in 2023.

- We are still optimistic, as we see the current price above the low of 2022, while the latter is above the low of 2020.

- It is hard to imagine copper prices going much lower in the long term, as discoveries of new copper deposits are limited while the world needs a lot of copper as electrical vehicles are gaining market share.

Chart courtesy of StockCharts.com

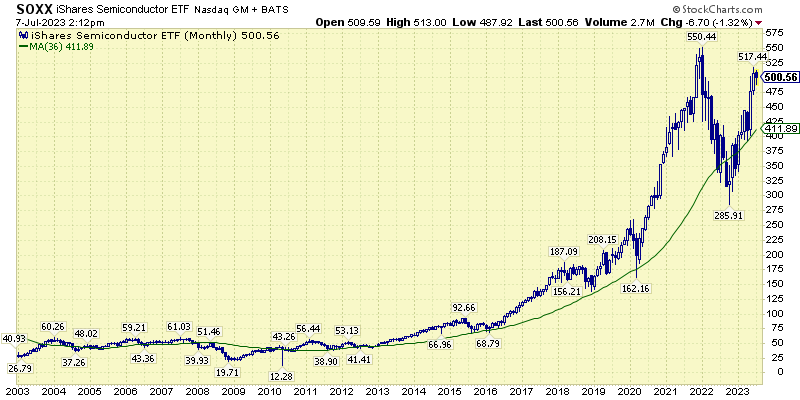

Dr. Semiconductor

Semiconductors, a more modern version of Dr. Copper, are reflecting what is happening in the most advanced parts of the economy.

- Semiconductor stocks are doing well, as seen in the chart below.

- Current strength is driven by the AI race and push for semiconductor independence.

- While the stock prices of the sector are short-term overbought and subject to U.S.-China trade war, we expect long-term strength in the sector.

Chart courtesy of StockCharts.com

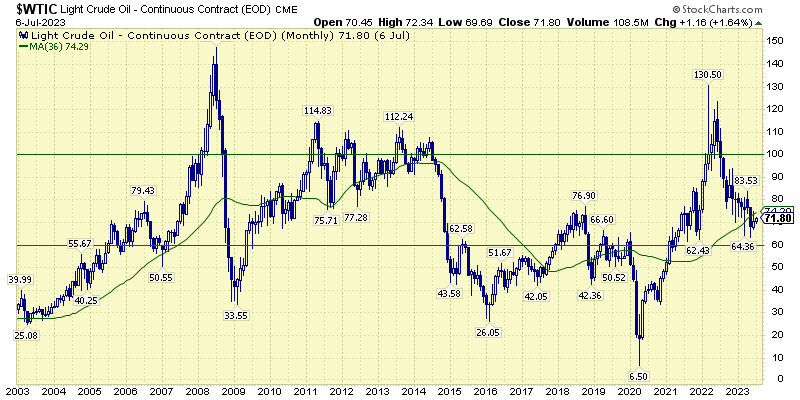

Energy

We expect U.S oil price (WTI) to stay in the wide range of $60-100 per barrel. Oil prices are volatile, like most commodities. We think it is unlikely to go below $60 during the next 3-6 years, considering the relatively low investments in production capacity in the past 10 years. We don’t expect it to go above $100, given the continuous efforts to transition to cleaner energy.

Chart courtesy of StockCharts.com

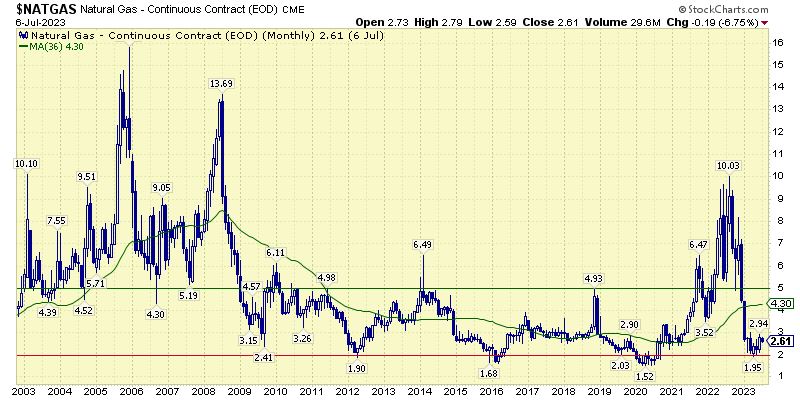

We expect U.S. Natural Gas price to stay in an even wider range of $2-5 per MCF (the gas prices are oscillating more than oil prices, due to exposure to the weather/heating season). We do not expect it to go lower than $2 since the world is transitioning from coal/oil consumption towards natural gas and other cleaner alternatives.

Chart courtesy of StockCharts.com

SECTOR POSITIONING FOR THE DIVIDEND VALUE DISCIPLINETM

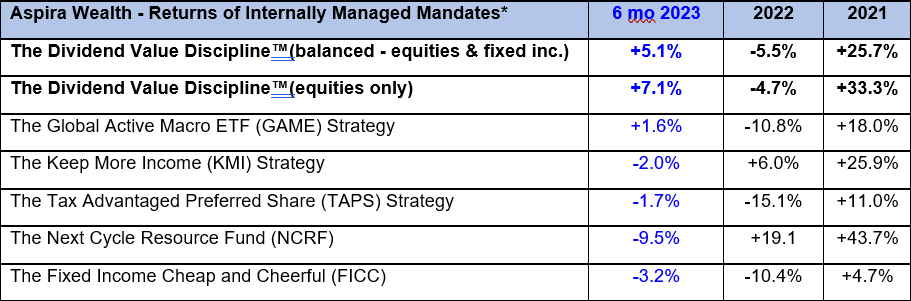

INVESTMENT PERFORMANCE

Most of our in-house investment strategies ended the years of 2021 and 2022 with significantly better results than the market averages. For the first half of 2023, our flagship investment strategy, The Dividend Value Discipline™ (equities), was up about 7.1 per cent, lagging moderately the market indices. The rest of the strategies returned between negative 9.5 per cent and positive 5.1 per cent, since the start of 2023.

Source: Aspira Wealth. *These numbers are relevant only for accounts with Raymond James Ltd. (Canada).

USEFUL LINKS

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd./Raymond James (USA) Ltd is not responsible for the availability or content of these external sites, nor does Raymond James Ltd/Raymond James (USA) Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd/Raymond James (USA) Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()