The Quarterly Opportunity Update – Transcript

Q3 2022

BY: Chris Raper, CFP®, CIM®

Audio Version

Track #1: Introduction – The Skinny

Track #2: The Markets – Blow-off Tops!

Track # 3: Our March North Continues – The Q3 2022 Recap

Track #4: Takeaways and Our Own Euro Style Energy Crisis

Track #5: Ukraine – Are We Ahead of Ourselves?

Track #6: Postscript I – The Aspira Wealth Approach

Track #7: Postscript II – The Dividend Value Discipline™ Methodology

Track #1: Introduction – The Skinny

Hi, this is Chris Raper, Wealth Advisor & Portfolio Manager with the Private Client Group of Raymond James Ltd. & co-founder of Aspira Wealth. Welcome to The Q3 – 2022 Quarterly Opportunity Update, which is being recorded for you on Thursday, October 6, 2022. For your awareness, this recording comes to you with a full transcript complete with charts/links that evidences the issues I will be speaking on – I believe you will get a lot more out of audio by referencing the transcript.

You are listening to Track # 1: The Skinny, where I am going to give you the high points on what we are going to cover today.

Track # 2: The Markets – Blow-off Tops! – I will start with a discussion on interest rates because they are ultimately the arbiter of stock valuations. Then I will follow our usual course speaking to our leading economic indicators, the energy complex and our Canuck buck, where the price action has been pretty much due south. In fact, it has been so bad that it can be seen as good. Obviously, that is a bit of a paradox so I will unpack that, speak to what I believe are blow-off tops and how that sets us up for a potential reversal of trend, in this case, to the upside!

Track # 3: Our March North Continues – The Q3 2022 Recap, I will cover where we landed with our core investment strategy, The Dividend Value Discipline™ on a year-to-date basis and how our march north (i.e., Canada and resources) has served us so well this year. I will also unpack the returns in our remaining 6 in-house strategies where the news has been mostly positive, at least on a relative basis. Put another way, we have not endured the full brunt of the current market selloff.

Track #4: Takeaways and Our Own Euro Style Energy Crisis

I will sum up the takeaways, and then speak to what is setting up to be the next Euro style energy crisis, but this time it will be in the renewables space and the vulnerability is global. As you might expect, we see both danger and opportunity and we are working on avoiding the former and exploiting the latter.

Track #5: Ukraine – Are We Ahead of Ourselves? I will speak the mainstream narrative on the current Ukraine/Russia war and offer some plausible alternative views which could surprise us. Ultimately, the unfolding events are going to have an impact on geo-politics and our capital markets, so it is incumbent upon us to challenge the groupthink.

Track #6: Postscript I – Our Approach is for the benefit of prospective clients. It will give you some insight on the new client process that we walk interested parties through. It starts with you and your story - our approach is tailored to your “do, have, and legacy” ambitions. In short, we need to understand your aspirations before we can help you achieve them.

On Track #7: Postscript II is where I walk you through the methodology and return objectives of our core program, The Dividend Value Discipline™. If you have an interest in the specifics of our core investment process, you will probably get a lot out of it – if that’s not you, you may want to give it a pass.

In terms of legal requirements, there are three things to note:

- The opinions that are expressed on this recording are mine. They may differ from those of Raymond James Ltd.

- Raymond James Ltd. is a member of the Canadian Investor Protection Fund. That is a good thing. If you are interested in those details, please ask me or any one of our relationship managers the next time we speak.

- The transcript of this recording provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd. endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd. adheres to.

I also want you to recognize that some of the things I am going to say today are going to be proven wrong. It is an inevitable part of this business. It is also important to recognize that you don’t have to be right all the time to do well. You just have to be more right than most or, conversely, less wrong than most.

Finally, regarding investment jargon, when I say I am bullish, it means I expect things to go up. When I say I am bearish, it means I expect things to go down. Likewise, north means up and south means down. When I speak about rent cheques, I am speaking about income, primarily dividends. You may hear me use the term “disruptor”, which is our moniker for companies that are disrupting or re-inventing the way business is done in their particular market and are thereby able to grow at rates far faster than those of the economy. Think of Wal-Mart twenty years ago and Amazon today. You may also hear me use the term “aggregator”, which is our moniker for companies that have a systemized approach to acquiring smaller competitors as a means to fuel their growth. That growth is the path to increasing dividends or in our language, growing rent cheques. If you catch me using industry jargon beyond that, I invite you to call me out. Send an email to the office and the team will let me know, usually with considerable gusto!

That’s a wrap on the skinny, and off we go to Track #2.

Track # 2: The Markets – Blow-Off Tops!

Starting with interest rates, as I outlined in our Timely Market Dispatch on Monday, September 26, 2022, stocks have a new competitor – with interest rates on GICs with terms of one to five years, knocking on 5% currently versus 2% a year ago, you can understand the attraction. As a side bar, make sure to take inflation and taxes into account - the headline number might not be as sweet as one would assume.

As we closed out Q3, the overwhelming consensus was that interest rates are going higher still as global central bankers fight inflation with the only real tool they have. Historically speaking, the one thing we know about the “overwhelming consensus” on virtually any market matter, is that when everyone agrees on direction X, it is almost always wrong. Why? Because humans tend to operate in groupthink mode and by the time everyone agrees, they have already adjusted for the said outcome and that sets us up for a sharp reversal.

As we closed out Q3, I believe we saw that phenomena being played out. The world’s benchmark interest rate, the yield on the 10 year US Treasury notes, ($TNX) went hyperbolic on Monday, Sept 26 and pegged 4.0% early Tuesday morning, then closed down sharply on the week at 3.8% and has fallen further, and 3.8% at the close of October 5th. This is classic behaviour for what is known as a “blow-off top” in the industry – it is a sign of panic from those being on the wrong side of the trade, which of course was the majority of market participants, because the overwhelming consensus was rates are going higher. Why is this important? To me, it means that rates may not be going a lot higher, that current rates are having the desired effect of dampening demand. I also found it interesting that the UK blinked on their path to higher interest rates last week. Couple that with some of the US Federal Reserve committee members musing about a possible slowdown in their increases and Australia signaling a pause and there is a good case to be made for at least a flattening of the trajectory. How does that impact us? I thought our Raymond James Institutional Equity Strategist, Tavis McCourt, said it well this past Monday, “it’s pretty simple at this point, 10-year Treasury yield goes up, and equities likely remain under pressure, it comes down, and equities rally.”

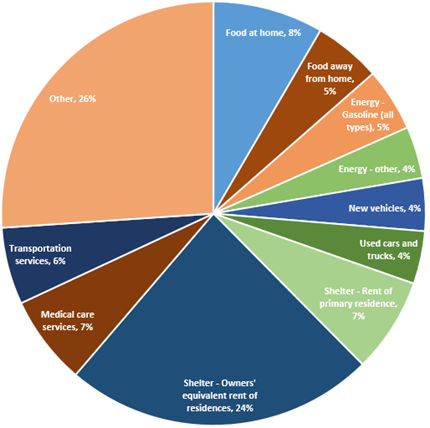

On the inflation front, there are some lower numbers in the cards. Recall that the reported consumer price indices are trailing indicators, they tell us what has already happened - when we look to what makes up the inflation numbers, we see that shelter (rent), food and transportation make up ~ 50%.

While I don’t have numbers for Canada, I can verify that rent costs in the US are falling like a stone – likewise, corn is ~ 15% off its high, wheat about 25% and $WTIC some 33%. It seems plausible that lower inflation numbers are in the cards, which pave the path for flat to down interest rates, which would be a definite positive for stock valuations. The market being a forward-looking animal, I believe we have seen that play out this week.

Source: Aspira Wealth / www.bls.gov

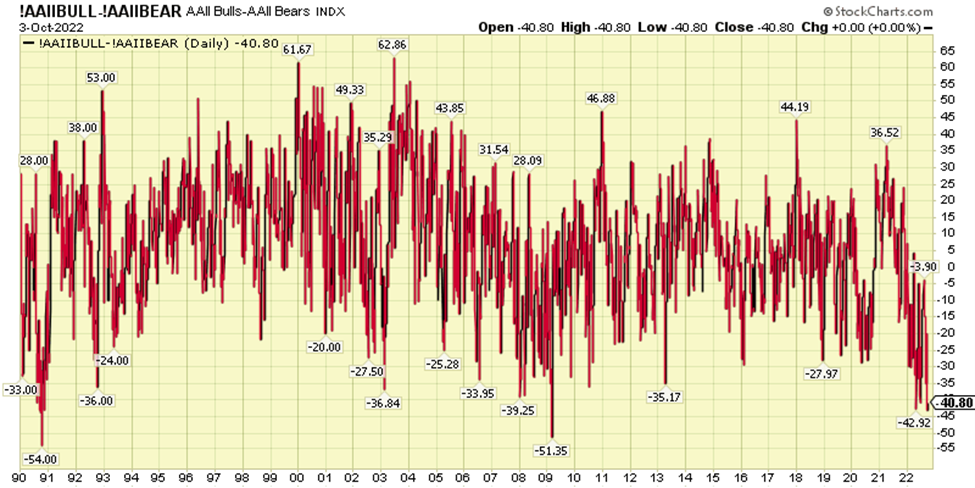

Couple the above with what I am seeing in the investor sentiment numbers, which can only be described as extremely bearish, and doesn’t matter if you look at retail or the professional crowd – the overwhelming consensus extreme fear and again, extreme groupthink is almost always wrong. Recall that these are contrarian indicators.

RETAIL SENTIMENT – the fear is at extremes and worse than during Covid 2020 and only exceeded in 2009

Charts courtesy of StockCharts.com

PROS SENTIMENT – fear levels amongst the professional crowd were higher than during peak Covid in 2020

Charts courtesy of StockCharts.com

Turning to our leading economic indicators, Dr. Copper, that shiny red metal that goes into virtually every manufactured good in the world and thus our vector for the world’s manufacturing economies, was at $3.32 per pound on the July 14, 2022 recording and today, it is pegging in at ~ $3.50. In other words, barely fogging up a mirror – no inflation here. Thankfully, it is up off its July and September lows so perhaps pointing to better demand in the months ahead, but too soon to tell.

Charts courtesy of StockCharts.com

When we turn our attention to our vector for human ingenuity based economies, the Philadelphia Semiconductor Index ($SOX), we see that it actually closed out Q3 at a new 2 year low. As was the case last quarter, the pattern of lower highs and lower lows, is suggesting slower growth ahead for our service based economies. Again, it supports the supposition of lower inflation and thus, perhaps somewhat lower interest rates ahead.

Charts courtesy of StockCharts.com

Turning to the energy complex, yes oil is off by a third from its high water mark back in March but it is well north of its subzero level in April of 2020. Our overly ambitious green energy agenda has translated into a severe curtailment in oil and gas production within western democracies where environmental standards are high, leaving regimes like those of Russia, Saudi Arabia and China to benefit while giving lip service to climate issues.

The disappointing thing is that Canada could have been at the forefront, and still can be, producing the most environmentally responsible energy on the planet while making billions of $’s for its citizens and government coffers. At the same time, we could be offering the world incremental improvement on the environmental front. For example, if Canada’s clean natural gas replaces coal in the energy mix, is that not a net gain? Ditto, for nuclear?

Bottom line, there is no quick path forward to solving the world’s high energy prices, it is a supply issue and thus we expect our oil and gas investments to continue to do well, notwithstanding our current political policies.

Charts courtesy of StockCharts.com

That brings me to our Canuck buck, where I could not have been more wrong. Many of you have heard me opine how it is really hard to keep the $CAD down in an energy boom, notwithstanding our current energy policies. That just hasn’t worked out. The reality is that the $USD Index has been a rip roaring terror as the world got attracted to their higher interest rates and the relative safety of the $USD. While that was going on, the loonie headed south in a big way. The only good news in this is it allowed us to sell our US securities and buy our Canadian resource stocks on the cheap, but anyway you shake it, I missed the mark by a wide margin.

Looking ahead, we may have seen another blow-off top in the $USD – again a hyperbolic move north as we close out the quarter (read panic) and we are currently well down on the week. My take is that we have hit the highs for the year and the $CAD will be higher by year end.

Charts courtesy of StockCharts.com

I will close out this track with Buffett’s well known quip, “be greedy when others are fearful” – make no mistake about it, investors both retail and professional were plenty fearful as they embraced one another’s’ group think. We prefer the opposite tack and with that we are off to Track #3.

Track # 3: Our March North Continues – The Q3 2022 Recap

By north, I mean Canada at the expense of US stocks and getting even more granular, we have favoured energy related stocks at the expense of technology related companies, which are domiciled in the Communications (Facebook/Alphabet), Consumer Discretionary (Amazon) and Technology sectors (Apple/Microsoft).

As you may have noted on the distribution link of this email, all eight out of ten of our largest rent cheque increases (dividend raises) this year have come from companies within the energy complex. A couple of weeks back I was presenting to the Victoria Estate Planning Council where I quipped, “some of you in the room have only seen technology stocks go up and commodity stocks go down – there is a simple reason for that – you have not lived long enough”. The point being, what we are witnessing today is very much akin to the post dot-com bubble. History often rhymes. I well remember some of my younger colleagues encouraging me to totally exit energy related investments and my retort then as it is now, was sometimes energy is the only thing that works. That has certainly played out thus far in 2022.

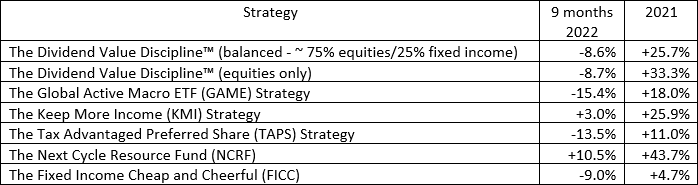

To exploit that phenomenon, our core program, The Dividend Value Discipline™ (DVD), owns a lot more energy related stocks today than it did say a year ago. We have also developed the all Canadian Keep More Income and Next Cycle Resource strategies to take advantage of the same. For the benefit of those in listen only mode, here is where our various in house strategies pegged in at the end of Q3 on a year-to-date basis with comparative numbers for the full year in 2021.

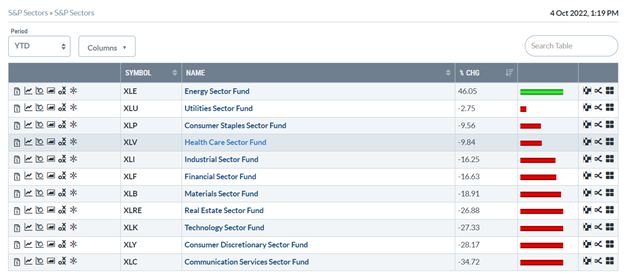

For some rough context, the S&P 500 pegged in at -25% in the first 9 months of 2022, while Canada’s S&P TSX was at -13%, so clearly the march north has helped in a big way. Most of the strategies experienced better returns on the quarter – not so for the major market indices.

Side bar disclaimers - those return figures do not include the returns from the non-discretionary side of your accounts. For most of our clients, that means guaranteed investment certificates (GICs) and the now more appropriately named high interest savings accounts (HISA). Our objective when owning the same is to make sure you never have to sell securities in a down market to meet your cash flow requirements.

Second side bar - the above numbers are only applicable to accounts we manage within the Raymond James Ltd. (Canada) platform. Our cross border clients who have accounts domiciled at Raymond James USA Ltd. will have different results, in large part due to currency swings.

Third and final side bar - the timing of cash flows and our buy-only approach for new money translate to considerable variability in actual client experience. For your awareness, the Sept. 30, 2022 statements are now up on your client login site. If you are not using that site, please reach out to us so we can get you up and running. We will kill less trees, it has 24/7 access and is far more secure than email.

That concludes Track #3.

Track #4: Takeaways and Our own Euro Style energy crisis

In staccato format, the takeaways:

The Skinny

- The opinions expressed are Aspira’s - they may differ from those of Raymond James Ltd.

- Some of what I told you is going to turn out to be wrong – witness what I said about the $CAD six months ago

- The charts and links are for your benefit – neither Raymond James nor Aspira is responsible for the content

The Markets – Blow-off Tops

- We believe we have seen the highs in the world’s benchmark interest rate and the $USD for 2022

- Lower inflation numbers are in the cards in the not too distant future

- Investors are terrified – it is time to be greedy, especially when it comes to Canadian resource companies

Our March North Continues – The Q3 2022 Recap

- Our migration from US stocks to Canadian stocks/technology stocks for resource stocks has helped shelter us from the worst of the current market selloff

- Our biggest rent cheque increase continues to come from our Canadian energy stocks

- We have seen this movie before in the post dot-com era – the cycles are long despite the setbacks – in our opinion, we are still in the early innings of the commodity ballgame

That takes us to our own pending Euro style energy crisis – one that could still be averted if our political leaders in the West were to turn their attention to it.

Here is what we, the people who elect them, need to be aware of. As we transition to renewables, we have ceded control of the upstream components to China. A point in case, China currently produces ~ 70% of the world’s solar panels and they use a lot of energy to do so, most of it from coal. When we look to other green components, China controls 80% of the world’s cobalt, not because they have the resource, rather they control the manufacturing and have global supply agreements. You cannot put Tesla’s on the road without cobalt and you can get cobalt without China processing it with coal fired electrical plants.

If that’s not bad enough our western democracies, including Canada, are letting the feedstocks to these industries slip through our fingers without much thought. To wit, The Globe and Mail’s article from August 13 last, China has encroached on Canada’s critical minerals industry, with almost no obstruction from Ottawa, where we let one of the world’s richest lithium deposits domiciled in Manitoba slip into Chinese control, seemingly with little thought as to the long term consequences. The National Post is also ringing the alarm bells with its recent articles on New World Disorder.

For those keen to read more, Raymond James put out a great piece on August 29 last, Could China Hold the Global Economy Hostage by Withholding Rare Earths?

Candidly, we are still trying to figure out how to protect ourselves and ultimately prosper from this phenomenon. One plausible outcome is that western democracies wake up and regain control of their supply chains. With or without that change, the owners of these base resources should do well. That bodes well for our current direction but standby for further thinking/action in the months to come. When it comes time to choose our next government, we should think carefully about who we are beholden to as we pursue our green initiatives, less we create our own Euro style energy crisis.

Track #5: Ukraine – Are We Ahead of Ourselves?

This discussion reminds me of the 7 Provocative Questions & A Shifting World Order piece I did on April edition of this recording. It won’t surprise you that we spend a lot of time weighing alternative views from mainstream thinking – the reason is pretty simple – historically speaking, mainstream thinking is often wrong and that is a pattern we do not expect to change – humans will continue to be humans. While many of our readers, ourselves included, have been buoyed by the recent gains of the Ukraine forces, we remain deeply disturbed with the humanitarian costs on both sides of the border. If your son gets killed in battle, I suspect it hurts equally, regardless if you are pro-Russia or pro-Ukraine.

What follows is a recap of what we believe is mainstream thinking and then some counter arguments. With apologies to those in listen only mode, we do supply links detailing the rationale for the alternate arguments.

Mainstream thinking: NATO will continue to bolster weapons and intelligence support to Ukraine until Russia withdraws.

- Reality: There are signs that perhaps the support is peaking, at least in the near term - the issue is supply chain – we just don’t have the industrial capacity to produce more weapons in the short order. Check out CNBC’s The U.S. and Europe are running out of weapons to send to Ukraine and Bloomberg’s US Is Sending More Artillery to Ukraine — But It Won’t Arrive for Years

Mainstream thinking: Russia is mobilizing mostly untrained people.

- Reality: Russia does have about one million of active personnel and two million of reserve personnel. Russia could plausibly move some active personnel to Ukraine from Russia’s non-active areas and replenish those non-active areas with newly mobilized people, and then train them for battle.

Mainstream thinking: Winter is coming and the intensity of battles will wane.

- Reality: Historically speaking, the Russian army has done very well in winter. It seems they are used to operating in harsh conditions. Recall that they launched major successful offensives in winter in WW II in 1941, 1942 and 1943 and more recently in the Donbas in 2015.

These challenges to mainstream thinking need to be weighed – it seems the situation in Ukraine might not get resolved as quickly as hoped and if that turns out to be the case, it makes for a worsening of geo-politics globally and even stronger demand for control of basic resources.

These are complex issues with no easy answers – that said, being aware of plausible outcomes from the mainstream can alert one to both dangers and new opportunities.

That brings us to a close for this edition of The Quarterly Opportunity Update. A reminder, if you are being introduced to us by way of this recording, then Tracks #6 and #7 are for you. Thank you for taking the time to listen. If you have people in your life who you think might benefit from these missives, please forward them as you see fit. Alternatively, they can sign up through our website, where all that is required is a first name and an email address. Alternatively, they can book some time at Book Appointments.

For now, this is Chris Raper, co-founder of Aspira Wealth, wishing you and your loved ones the very best for the Thanksgiving holiday – as we gather for our feast this weekend, please join my family and me in praying for a better world. Good day and may God bless from Victoria B.C. on Thursday, October 6, 2022.

Track #6: Postscript I – Our Approach

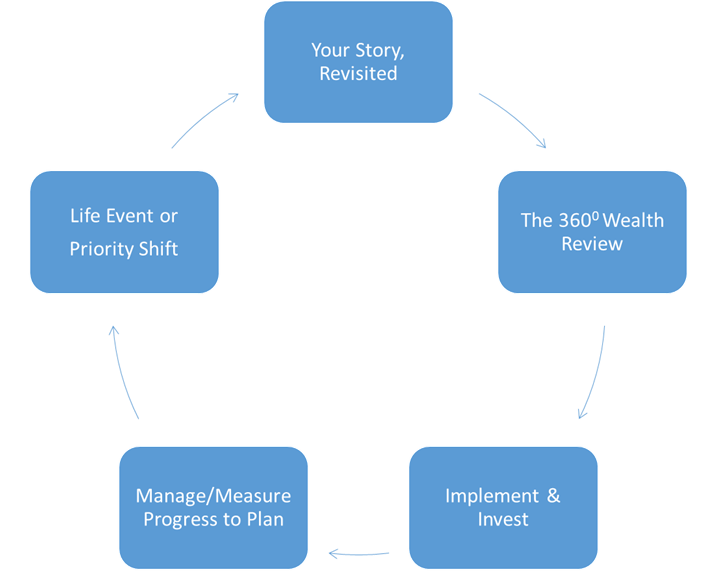

While this recording has been focused on investments that is not where we start with new relationships. We start with your story, and we revisit it often. Knowing where you came from and what you want the future to look like – your do, have, and legacy ambitions – is the foundation for building a solid client/wealth advisory relationship. Our first order of business is to listen, seek clarity and then document your ambitions for the future – we call it, Your Story, Revisited.

From there, we complete a 360⁰ review of all relevant investment, tax/estate and insurance documents in an effort to identify gaps/risks to the future you envision. When we identify holes, we have a discussion about how we might fill those holes.

Then and only then do we get into a discussion on the investment allocation. We will address your liquidity, income and growth requirements/desires and introduce you to the tax smart investment strategies to meet those needs.

After we invest, it is a matter of manage and measure – we report regularly and when life throws you the inevitable curve ball or your priorities change, it is back to revisiting your story.

In summary, we learn about you, your family, your finances and what your ideal future looks like – the things you want to do, the things you want to have and the legacy you want to leave. We identify the structural risks and how we see mitigating them. We paint a go forward picture with a worst case analysis of the costs involved.

Generally speaking, we are looking to establish relationships with new clients that have north of $1 million in investable assets, but please understand that we are a lot more interested in where you are going than where you are. If you have a credible plan to get to that number say within a three to five year period, we are very interested in meeting with you.

So…if that process sounds engaging, I invite you to call and book some time. If you’d like further information, including access to our quarterly communication pieces, you can check us out on the web at www.aspirawealth.com and send us an email from there.

Track #7: Postscript II – The Dividend Value Discipline™ Methodology

The first thing I want to share with you is that The Dividend Value Discipline™ is our core mandate – essentially, all of our clients have a slice of their portfolio allocated to it. For your awareness, we currently have several strategies that we manage in house, in addition to a short list of 3rd party money managers. Structurally, most clients have three buckets of money with us – a safe money bucket, an income bucket and a growth bucket. The Dividend Value Discipline™ straddles the latter two and depending on your needs, we augment it with other strategies. The program continues to be a large slice of our client assets under management and in my case, it is by far the largest.

The process is discretionary, meaning we make all of the buy and sell decisions and report to you after the fact.

Our objectives for the program are:

- Income every month – that can be paid out or reinvested;

- An acquisition process where we buy only those securities which become attractive on a “go forward” basis;

- Absolute returns of 8%+ over any investment cycle, which we would describe as peak to peak or trough to trough. If you are looking for a time frame in terms of years, think 5+ years, but please understand investment cycles have a wide range of timeframes.

The program operates with three key elements and I will walk you through them using the illustration of a three legged stool.

The First Leg Is Dividends

With few exceptions, every security that we buy must provide some form of income. We do that because income makes portfolios inherently less volatile, i.e., less chance of loss. The analogy I like to use is that of an apartment block versus a piece of raw land – it is a lot easier to hold on to an apartment block in a tough real estate environment when you are getting a rent cheque every month. Income drives stability and absolute returns.

The Second Leg Is Value

Our research function is in house. When we launched the program back in September of 2002, we were one of the first private client teams in the industry to have a dedicated analyst on staff and we add additional resources every year. We spend an inordinate amount of time studying the corporate culture of potential investee companies. If you are interested in what great corporate culture looks like, I encourage you to read Good to Great by Jim Collins – that is the yardstick we use to measure potential investments against. Another yardstick is the importance of wide economic moats – the things that make the company tough to compete with. We want to own companies that the end client can’t live without – great examples might be Microsoft or Intuit, both long term holdings of ours. We believe that the focus on great corporate culture and wide economic moats gives us an edge, and while I can’t prove it to you, I can certainly give you lots of anecdotal evidence to support that thesis.

The more recent development in our strategy has been tackling the growth problem. History buffs will note that when we started the program in 2002, we had 5-year GICs yielding roughly 5% and much better economic growth, whereas today we have 5-year GICs yielding ~1.5% and much slower economic growth. In short, the 8% is tougher to come by.

Accordingly, we spent late 2015 and 2016 tackling the growth problem. We needed to find companies that were growing far faster than the economy. As you would expect, we started within the normal confines of “has to pay a rent cheque, score well on the corporate culture front and have some sort of strategic advantage (moat) that makes the company difficult to compete with”. We then focused on companies that have demonstrated their ability to grow their earnings/dividends at double-digit rates as a primary indicator of income growth and capital gain potential. As we searched, we found that most such companies fell into one of two themes. They tended to be disrupting the existing marketplace (think Wal-Mart 20 years ago or Amazon today) with a better way of doing things, and/or they tended to be aggregating their way to growth by buying smaller tuck-in acquisitions, much like Constellation Software Inc.

The Third Leg Is Discipline

Here I refer to the buy/sell decisions.

On the buy side, I would sum it up as “do your homework, be ready, be patient”. Over the years, our absolute best buys have been when we have done our homework on the company, perhaps months before, and then some untoward event happens that gives you opportunity to buy in size. The Euro debt crisis in 2011 is a great example that enabled us to buy Nike at a terrific price because we were ready and we had conviction. More recently, I would put the world’s #3 French fry maker, Lamb Weston, in that category.

Sell decisions are getting increasingly tougher because the quality of our companies just keeps going up and with their rent cheques (dividends) growing at double-digit rates, our history tells us more often than not that we are better off holding than chasing shiny baubles. That said, new competitors with disruptive technologies can wreak havoc on a company’s growth prospects – back to the Amazon/Wal-Mart example. Transition periods of senior management teams can be risky, especially when there is no hire-from-within bias. Then there are times when the price of a stock just gets so far in front of its growth prospects that the only reasonable thing to do is sell. As Buffett likes to say, “You pay a high price for a rosy consensus”. When things are universally rosy, we try to be sellers, not buyers.

Perhaps the most important part of the buy/sell discipline is the way we operate the program for new entrants – we call it “The Buys Only Mandate”. Unlike most of our competition, we only buy securities which become attractively priced on a go-forward basis, meaning if you start today and your brother starts three months from now, your portfolios are going to be different in the short-term, and more closely aligned the longer you are in the program together. As rational as that might seem, most people do the exact opposite. Every time you buy a mutual fund, you buy a pro-rata share of an existing portfolio – by definition, you got the buys, the holds and the near sells. To us, that is not rational. Who buys 100+ companies in a single day? Were they all great value propositions? You should also be aware that most third party money management programs work exactly the same way – they buy the basket. The buys only mandate was designed to protect your hard earned money.

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()