The Quarterly Opportunity Update – Transcript

Q4 2022

BY: Chris Raper, CFP®, CIM®

Audio Version

Track #1: Introduction – The Skinny

Track #2: The Markets – Take Comfort In The Overwhelming Pessimism

Track # 3: Dividend Gushers & The 2022 Performance Recap

Track #4: Tumbling Titans – There Are Better Alternatives

Track #5: The Wrap Up & Key Takeaways

Track #6: Postscript I – The Aspira Wealth Approach

Track #1: Introduction – The Skinny

Hi, this is Chris Raper, Wealth Advisor & Portfolio Manager with the Private Client Group of Raymond James Ltd. & co-founder of Aspira Wealth. Welcome to The Q4 – 2022 Quarterly Opportunity Update, which is being recorded for you on Tuesday, January 17, 2023. For your awareness, this recording comes to you with a full transcript complete with charts/links that evidences the issues I will be speaking on – I believe you will get a lot more out of audio by referencing the transcript.

You are listening to Track # 1: The Skinny, where I am going to give you the high points on what we are going to cover today.

Track # 2: The Markets – Take Comfort In The Overwhelming Pessimism

There are few things market wise that give me more conviction than an overwhelming consensus, be it positive or negative, and it is the latter where we find ourselves at the end of 2022 – read opportunity knocks. I will give you the evidence that supports that supposition and then we will walk through the inflation/interest rate debate, our leading economic indicators, and the commodities complex. Our take? The recession/slowdown is already behind us and or at the very minimum, is already priced in. Either way it is bullish for stocks.

Track # 3: Dividend Gushers & The 2022 Performance Recap, we will highlight the top 5 dividend increases for both The Keep More Income Strategy and The Dividend Value Discipline™, and what a year we have had on that front. Then we will cover off the year end performance numbers with some expanded colour as to how we achieved those results.

Track #4: Tumbling Titans – There Are Better Alternatives, I will speak to why I believe the 2022 dismal performance in mega technology companies will continue to exhibit ongoing selling pressure in 2023.

Track #5: The Wrap Up & Key Takeaways

On track #5 I will wrap it up with the key takeaways and let you know how to introduce us to those people you believe we can help.

Track #6: Postscript I – Our Approach is for the benefit of prospective clients. It will give you some insight on the new client process that we walk interested parties through. It starts with you and your story - our approach is tailored to your “do, have, and legacy” ambitions. In short, we need to understand your aspirations before we can help you achieve them.

In terms of legal requirements, there are three things to note:

- The opinions that are expressed on this recording are mine. They may differ from those of Raymond James Ltd.

- Raymond James Ltd. is a member of the Canadian Investor Protection Fund. That is a good thing. If you are interested in those details, please ask me or any one of our relationship managers the next time we speak.

- The transcript of this recording provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd. endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy, which Raymond James Ltd. adheres to.

I also want you to recognize that some of the things I am going to say today are going to be proven wrong. It is an inevitable part of this business. It is also important to recognize that you don’t have to be right all the time to do well. You just have to be more right than most or, conversely, less wrong than most.

Finally, regarding investment jargon, when I say I am bullish, it means I expect things to go up. When I say I am bearish, it means I expect things to go down. Likewise, north means up and south means down. When I speak about rent cheques, I am speaking about income, primarily dividends. If you catch me using industry jargon beyond that, I invite you to call me out. Send an email to the office and the team will let me know, usually with considerable glee!

That’s a wrap on the skinny, and off we go to Track #2.

Track # 2: The Markets - Take Comfort In The Overwhelming Pessimism

As we closed out 2022 and opened 2023 both the retail crowd and professional investors had a bonfire going in the camp of FEAR – false expectations appearing real. The story went something like this: inflation is rampant with no end in sight, interest rates will continue to rise and people will lose their homes, people can’t afford to eat, energy costs are through the roof, the recession is coming and it is going to be a doozy, aka sell, sell, sell.

To wit, the National Post’s top story on Jan. 9/22 was Buckle up Canada, the recession has arrived. The article opened with “It’s basically unanimous that whatever Canada’s economic foibles are right now, they’re almost certainly going to get worse.” They then went on to report a recent Leger poll found that 81 per cent of Canadians suspect a recession is coming, and 56 per cent are actively preparing for it. Here is what I want you to take away from that. If 81% of any group is in full agreement on a given outcome, it is very unlikely to happen – simply put, that’s just not how the world works.

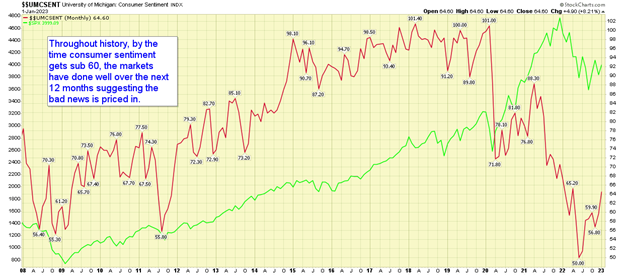

When we look south of our border, we get a similar picture. The Michigan Consumer Sentiment Index pegged a multi-decade low of 50 last summer, which incidentally corresponded to inflation’s peak rate, and that same sentiment index closed out the year sub 60. Here is what history has to teach us about such readings – the bad news is priced in. Over the last 50 years, market returns 12 months forward from such levels have averaged north of 20%.

Charts courtesy of StockCharts.com

What follows are the metrics that refute many of those fears.

First up, inflation is cooling – the US pegged in at 6.5% in December versus 9.1% when I reported to you last July, with the bold claim that Inflation Has Peaked. Even the Europeans are seeing far less inflation. When we look at all the major components that make up the Consumer Price Index, be it shelter cost, food inputs, or transportation, most are heading south and or significantly off where they were six months ago.

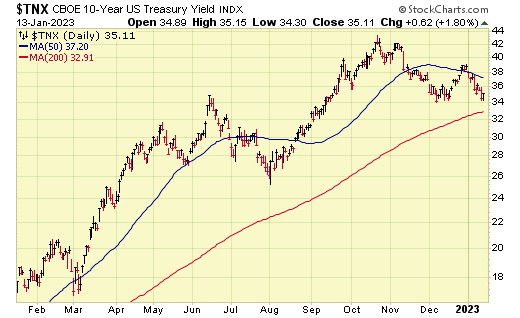

Interest rates – the world’s benchmark, the 10 year US Treasury Yield ($TNX), is now sub 3.50% after peaking at 4.25%. That has translated into marginally cheaper mortgage rates and the current trend is still south, albeit slowly. Notwithstanding the aggressive US Fed speak of higher for longer, three of their biggest hawks (the members likely to vote for higher rates), lose their votes in 2023. Like inflation, our take is that interest rates will be flat to down by the time summer vacations start.

Charts courtesy of StockCharts.com

If inflation is cooling and long-term interest rates are coming down, doesn’t that point to a recession?

While that is plausible, I don’t believe it is probable and here is why. When I look at our leading economic indicators, Dr. Copper, that shiny red metal that goes into virtually every manufactured good in the world and thus our vector for the world’s manufacturing economies, it has rocketed to north of $4.20 per pound versus $3.50 on our last October recording. It is screaming no recession.

Charts courtesy of StockCharts.com

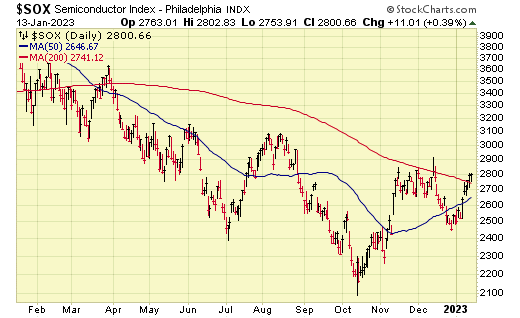

When we focus our attention to our vector for the human ingenuity based economies, the Philadelphia Semiconductor Index ($SOX), one can see that the two year low of last October is now only a painful memory and it is currently busting north, although less convincing than Dr. Copper.

Charts courtesy of StockCharts.com

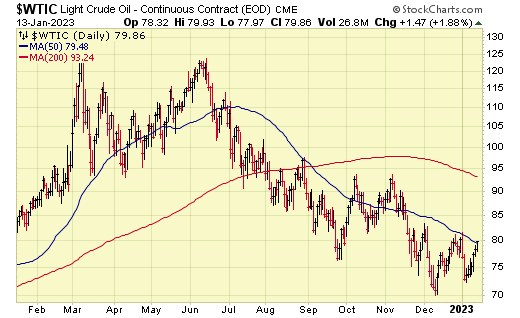

Turning to the energy complex, oil clearly took a breather in the last few months of 2022, while natural gas seemed to stop breathing, given Europe’s summer-like weather this winter. Their governments also deserve credit for their newfound willingness to pivot from Russian energy sources.

Charts courtesy of StockCharts.com

Those lower prices have eased the inflation factor and thus greased the wheels of commerce, which is another vote for no recession.

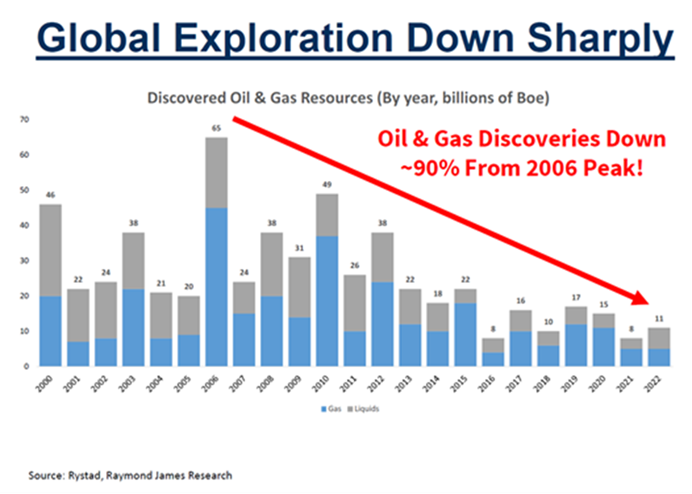

On a side note, I believe it will serve us well to recognize that we are still in a long-term energy supply crunch. To wit, global oil discoveries peaked at ~ 65 Billion BOEs (Barrel of Oil Equivalent) in 2006 – last year they were 11B. Is that because we don’t need the stuff? The data does not support that supposition – notwithstanding all our renewable efforts, global oil demand is still increasing by ~ 2 M BPD (Barrels per day), or pretty close to ¾ of a billion per annum. As China reopens and the US starts refilling their Strategic Petroleum Reserves, we expect demand to increase and with no apparent new supply, prices will likely rise. Bottom line, let’s not get too bearish on the oil and gas sector.

The last issue that I want to speak to is the continuing southbound trajectory of the $USD. On the October edition of this recording, I spoke to what I believed was a blow off top in the $USD Index at the 114 level – obviously, we don’t always get it right but we nailed that one. Here is why the lower USD is so important. For everybody X-USA, it means life gets cheaper - cheaper to pay USD denominated debt, cheaper to buy commodities, cheaper to buy US manufactured goods, which tend to be high precision machines, i.e. capital investments. In other words, it greases the wheels of commerce and here again a vote against the recession that everyone expects.

Charts courtesy of StockCharts.com

Of course USD$ weakness leads to $CAD strength and we are seeing that in the early days of 2023. Some of you will recall that I spent most of 2022 expecting a higher loonie and I was just way too early, aka wrong.

So let’s review – 2022 saw the S&P 500 down some 18%, that is rare. Most investors are worried about a doozy of a recession, yet most of the leading indicators are saying it is already behind us or were not going to have one anytime soon.

My take - I believe we will better served by taking comfort in the overwhelming fear – aka send some of that cash you have been squirreling away and we are off to track #3.

Track # 3: Dividend Gushers & The 2022 Performance Recap

I chose an oilfield analogy to highlight our biggest dividend increases this year because it was the oil and gas sector that delivered our biggest rent cheques, and wow, did they deliver. Let’s also recall that these same companies produce some of the most environmentally sensitive oil and gas on the planet. Yes, a shameless plug for Canada’s energy industry.

To wit, our top five increases in the all Canadian domiciled Keep More Income Strategy are as follows: Cenovus pegged in with a 200% year over year rent cheque increase, followed by Prairie Sky at 167%, Birchcliff Energy at 100%, Whitecap Resources at 63%, Freehold Resources at 50%. Canadian Natural Resources gets an honourable mention, at 45% and a special dividend per share of $1.50 to boot.

Turning to our top 5 in the Dividend Value Discipline™, while it wasn’t dominated by energy, our energy producers remained a significant contributor. Leading the pack was Mueller Industries with a 92% increase, followed by Tractor Supply at 77%, John Deere at 58%, Arc Resources at 50% and our longtime favourite, Tourmaline Oil Corp. at 39%, plus a total of $7.00 in special dividends throughout the year. Talk about a gusher. Just last week they announced their intention to move the special dividends to $8.00 in 2023.

Those rent cheque increases are just marginally above the rate of inflation and of course, that is important as we try to protect our purchasing power in this inflationary environment.

Moving to our year-end results, we released our performance numbers on Friday, January 6, 2023 for each of the in-house strategies we operate. Please be reminded that most listeners have a blend of those strategies and that the timing of cash flows, and our buys only approach when you add new cash, result in considerable variability in your household aggregate number. For your awareness, your household performance reports are now up on your client login site – if you are not using that site, please reach out to us so we can get you up and running. We will kill less trees, it has 24/7 access and is far more secure than email or snail mail.

What follows is a recap of the 2022 performance, by strategy, in decreasing order of total $’s committed to each program.

Starting with our long tenure core strategy, the Dividend Value Discipline™ (equities only) pegged in at -4.70% for 2022 versus a +33.3% in 2021. The takeaway is that we held on to most of the 2021 gains in a very tough year. Our resource exposure was the driving force behind that outperformance.

The Keep More Income Strategy, pegged in at +6% for 2022 versus 33% for 2021. Here again, the driving force behind our outperformance was the resource exposure. Please recall that the strategy is all Canadian, and due to Canada’s eligible dividend tax credit, our rent cheques received, are super tax efficient. If you need more colour, please reach out to us.

The Global Active Macro ETF (GAME) Strategy had a tougher year at -10.8% versus +18.0 the year prior. There is no question that the higher volatility last year made for some challenging trade decisions. That said, the system did keep us out of the technology behemoths that were the major cause behind the -18% decline in the S&P 500 last year. We stick with the strategy, recognizing that every process will have its season in the sun.

Next up in terms of $’s committed is our Fixed Income Cheap & Cheerful, which simply put, wasn’t very cheerful last year. A -10.4%, versus a 4.7% gain in 2021. As you are no doubt aware, bonds/fixed income got crushed this year as interest rates continued to ramp higher. By way of ETF proxy comparisons, the Canadian Aggregate Bond (VAB.TO) -11.9% and the US based US Aggregate Bond (AGG): -13.0%. The other thing to recognize is that for most clients, it is a relatively small part of your aggregate portfolio. The bright side is that the same selloff makes for a considerably more attractive entry point as we enter 2023.

Similarly, our Tax Advantaged Preferred Share (TAPS), which is also in the fixed income space, pegged in at -15.1% versus an 11% gain the year prior. There are two silver linings in that cloud:

- The dividend stream was ~ 5%, which is akin to say +7% in interest income, assuming you are in BC’s highest tax bracket. If taxable income is below $53000 per annum and Canadian eligible dividends are your only source of income, you get them tax free!

- We were able to crystallize the book losses prior to year-end by selling all the individual positions and buying Horizons Active Hybrid Bond and Preferred Share ETF (HYBR). That means we will be able to recapture taxes paid on our extraordinary 2021 gains.

Like the bond market overall, that 2022 selloff is making for an ideal entry point in the pref share space as we enter 2023.

Our Next Cycle Resource Fund continued to lead our performance numbers, pegging in at a +19.1% versus +43.7% in 2021, notwithstanding the collapse in oil and natural gas prices from the highs of last summer. We are still of the opinion that we are in say the bottom of the second inning of a nine inning game. While everybody is focused on the next recession, we encourage you to think through the inevitable economic recovery and the ever-tightening global energy supply in the face of that increased demand.

Track #4: Beware of TUMBLING TITANS – THERE ARE BETTER ALTERNATIVES

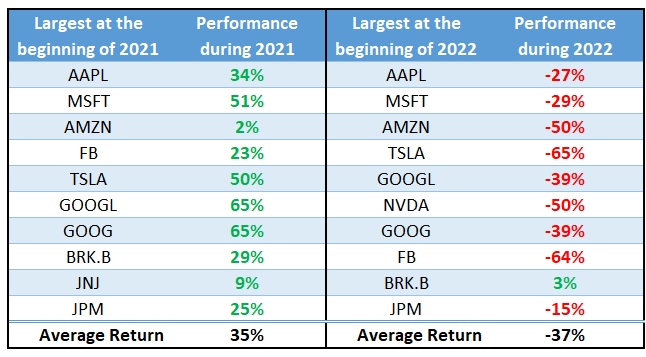

I feel compelled to speak on what are commonly known as mega cap stocks, the most valuable public companies in the US, in hopes of saving some listeners a lot of pain. I want you to think of the FAANG stocks, Facebook (now Meta), Apple, Amazon, Netflix and Google (now Alphabet) and major companies like them.

A quick glance of their performance over the last 2 calendar years reflects a crazy high return in 2021 and a house of pain in 2022. Given such a selloff, and when you think about how dominant each of the companies are, the 5 and the 10 year returns of such companies, it is very tempting to see the likes of AMZN and TSLA as bargain basement, can’t lose propositions.

Source: Aspira Wealth

As a group, I don’t believe that is the way it will turn out and here’s why:

- These companies have been accumulated by investors for years and now dominate most portfolios, ours excluded. In industry parlance, they are over-owned.

- Their growth prospects are deteriorating rapidly – witness the huge layoffs have been announced and we are only getting started. If you are a software engineer, you are in recession. Not true if you are a petroleum engineer.

- For the most part, these behemoths have been unfettered by regulation – that is changing, which further exacerbates their growth problem.

The whole environment reminds me of the implosion of technology stocks, circa 2000, and yes, I did make the mistake of buying into technology funds after that crash. I believed that they would promptly return to growth - little did I know that it would take 10 years! I watched those funds languish and lose money while smarter investors had moved to sectors, which had been starved for capital for years, i.e. oil, metals and industrials. I finally threw in the towel and joined them – I want to save you from a similar outcome. My hope is that those listeners who have a DIY side account will save themselves some money and for you baby boomer parents (and maybe even some Gen Xers), please send this note to your adult children and have them reach out to us if we can help.

Charts courtesy of StockCharts.com

Track #5: Wrap up and Key TakeAways

- Please be reminded that the opinions expressed are mine, they may differ from Raymond James Ltd and undoubtedly, some of them are going to be wrong. It is just a natural outcome of this business. When we are wrong, we fess up and move with the evidence.

- On Track # 2: The Markets – Take Comfort In The Overwhelming Pessimism because it generally means that all the bad news is priced in. With the S&P 500 down some 18% last year there is ample evidence to support that claim – it is also important to note that our leading indicators are suggesting that there will be no recession and that cheaper commodities, lower interest rates and a falling $USD, is greasing the economic output machine. Embrace the fear and find some money to invest.

- On Track # 3: Dividend Gushers & The 2022 Performance Recap, we spoke to the exceptional rent cheque increase we have had across the platform and most of them have been domiciled in the oil and gas industry. To be clear, I expect the 2023 increases to be far less spectacular. Our energy investments were the main reason for our relative outperformance last year, while we had a tougher time in the fixed income space. It is the latter where we are currently seeing some opportunity.

- On Track # 4: Beware of Tumbling Titans was essentially a recap of Investor Behaviour 101. Suffice to say we are extremely wary of buying the mega cap stocks, which put in dismal performances in 2022 – we believe you should be too.

- Track #5: Postscript I – Our Approach is for the benefit of prospective clients. It will give you some insight on the new client process that we walk interested parties through. Spoiler alert – it starts with you and your story - our approach is tailored to your “do, have, and legacy” ambitions. In short, we need to understand your aspirations before we can help you achieve them.

That brings us to a close for this edition of The Quarterly Opportunity Update. A reminder, if you are being introduced to us by way of this recording, then Tracks #5 and #6 are for you. Thank you for taking the time to listen. If you have people in your life, who you think might benefit from these missives, please forward them as you see fit, or even better introduce us via email and we will run with it from there. This is Chris Raper, cofounder of Aspira Wealth, wishing you and your loved ones all the best - good day and May God Bless from Victoria B.C. on Tuesday, January 17, 2023.

Track #6: Postscript I – Our Approach

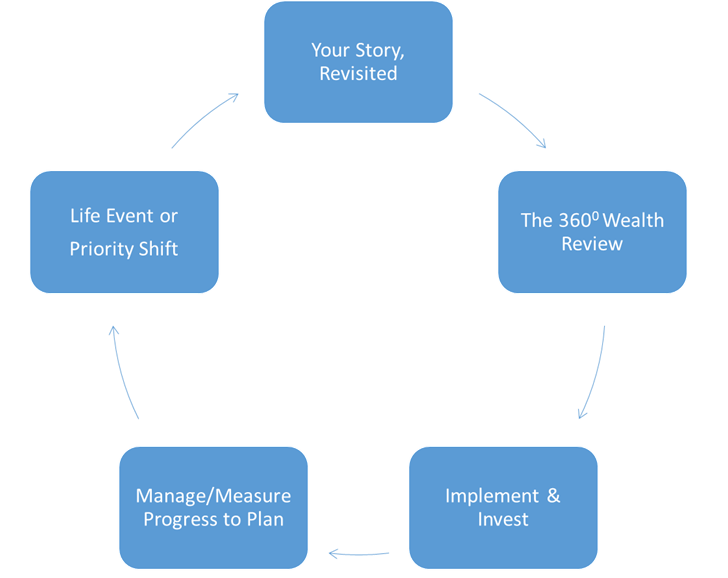

While this recording has been focused on investments that is not where we start with new relationships. We start with your story, and we revisit it often. Knowing where you came from and what you want the future to look like – your do, have, and legacy ambitions – is the foundation for building a solid client/wealth advisory relationship. Our first order of business is to listen, seek clarity and then document your ambitions for the future – we call it, Your Story, Revisited.

From there, we complete a 360⁰ review of all relevant investment, tax/estate and insurance documents in an effort to identify gaps/risks to the future you envision. When we identify holes, we have a discussion about how we might fill those holes.

Then and only then do we get into a discussion on the investment allocation. We will address your liquidity, income and growth requirements/desires and introduce you to the tax smart investment strategies to meet those needs.

After we invest, it is a matter of manage and measure – we report regularly and when life throws you the inevitable curve ball or your priorities change, it is back to revisiting your story.

In summary, we learn about you, your family, your finances and what your ideal future looks like – the things you want to do, the things you want to have and the legacy you want to leave. We identify the structural risks and how we see mitigating them. We paint a go forward picture with a worst case analysis of the costs involved.

Generally speaking, we are looking to establish relationships with new clients that have north of $1 million in investable assets, but please understand that we are a lot more interested in where you are going than where you are. If you have a credible plan to get to that number within a three to five year period, we are very interested in meeting with you.

So, if that process sounds engaging, I invite you to call and book some time. If you’d like further information, including access to our quarterly communication pieces, you can check us out on the web at www.aspirawealth.com and send us an email from there.

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd. is not responsible for the availability or content of these external sites, nor does Raymond James Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()