THE QUARTERLY COMPASS - ASPIRA WEALTH – Q2 2025

In-depth stock market analysis from your wealth advisory team - Aspira Wealth from Victoria, BC. Written by Alex Vozian, co-founder, and portfolio manager of Aspira Wealth.

Summary:

- THE FACTS: U.S. and Canadian markets had an impressive recovery in Q2 2025 ...

- THE NOISE: ... despite an overwhelming amount of uncertainty on multiple fronts

- OUR TAKE: While U.S. policy risks are diminishing overall (with occasional surprises like new Trump 35% tariff threat for Canada), the markets might be getting ahead of themselves.

- THE PLAN: Staying calm and rational amid today’s relentless noise

- TEAM UPDATE: CRPC, CSC, charity, mentoring, teamwork, soccer, golf, cycling, road trip, parents, kids

THE FACTS

Fear and Greed – the fear index level (VIX Volatility Index) is at a 5-month low level (i.e. investors are greedy), and CNN Fear & Green Index has just entered the “Extreme Greed" zone.

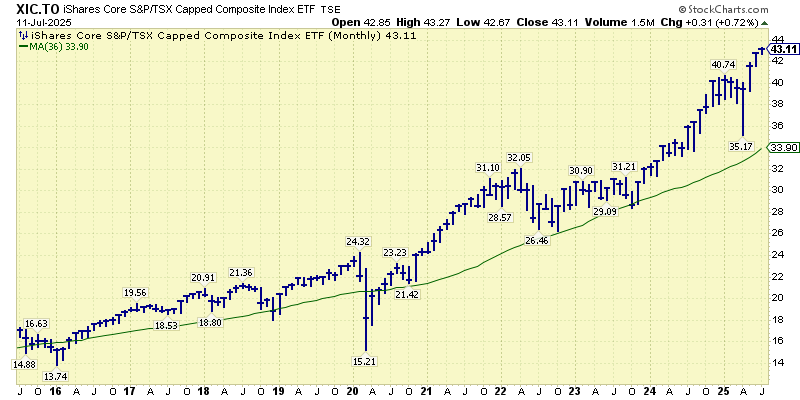

Canadian Stock Market – contracted sharply in April 2025, falling 14% under the 2025 record high, but then rallied more than 22% and reached new record levels.

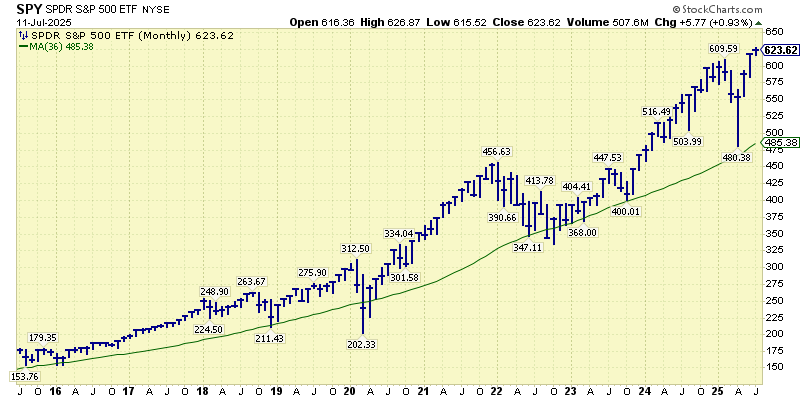

U.S. Stock Market - contracted sharply in April 2025, falling 21% under the 2025 record high, but then rallied more than 30% and reached new record levels.

Chart courtesy of StockCharts.com

Canadian 10-year bond rates – currently near one-year high level, after approaching the two-year record lows in early April.

U.S. 10-year treasury rate – currently near the mid-point of the two-year range.

USD CAD Exchange Rate – USD depreciated compared to CAD during the first half of 2025, moving closer to the middle of the 10-year range of $1.2-$1.5.

Copper Price - leading indicator for the “old” economy – rallied in Q2 2025 and hit a new record level in early July 2025. Trump’s threat on copper import tariffs had an obvious impact.

Semiconductors stocks – leading indicators for the “new” economy - Semiconductor ETF (SOXX) increased 66% from April 2025 low and is now close to the record level from 2024.

U.S. Crude Oil prices – dipped below our expected range of $60-100 in April-May 2025 but has quickly recovered above the $60 level.

U.S. Natural Gas prices – contracted ~30% from the two-year record high (achieved in March 2025) and is currently the bottom half of our expected range of $3-5 per MCF.

The NOISE

Second quarter of 2025 had a “big and beautiful” amount of noise. So scary that even the calmest people had occasional panic. So broad-based that it is hard to wrap your head around. So dynamic, with occasional 180 degree turns even in a single week.

Below are just some of the recent worrisome developments from the last months.

Trade & Tariffs – Extreme Uncertainty

- Escalating U.S. tariffs triggered global trade tensions and market volatility

- Reciprocal tariff threats from China, EU, and Canada led to policy instability

- Exemptions, delays, "deadline extensions", and legal challenges added confusion

- Exporters faced compliance burdens and scrambled to diversify suppliers

- Tariffs disproportionately affected lower-income people and consumer prices

Macroeconomic Fragility & Fiscal Stress

- U.S. budget deficit and interest payments sparked sustainability concerns

- The “One Big Beautiful Bill” raised concerns about rising debt

- U.S. GDP contracted in Q1, intensifying recession fears

- Inflation expectations rose despite muted real inflation

- Canadian unemployment hit 7%, highest since 2021

Business & Market-Level Pressures

- Businesses scrambled to front-load imports ahead of tariff hikes

- Retailers/manufacturers faced pricing dilemmas from tariff pass-through

- Mid-sized firms struggled with debt and credit access constraints

- Earnings guidance began reflecting inflation and trade pressures

- Predictability in tax policy eroded, harming business planning and capital spending

Geopolitical Risk & Institutional Breakdown

- Middle East tensions raised concerns over energy supply routes

- Domestic deregulation and fiscal policy threatened long-term stability

- Institutional trust eroded - concerns emerged about rule of law and governance

- Science, healthcare, and education funding cuts risked workforce quality

- Cuts to science and tech funding could undermine long-term innovation

Structural & Policy Concerns

- The broader policy pivot toward isolationism prompted re-evaluation of U.S. exceptionalism

- Global investors began pulling away from U.S. assets amid dollar volatility

- Immigration controls may limit reindustrialization capacity

- Immigration policy deterred talent inflow, hurting growth prospects

- Stable currency threatened by political pressure on the Fed

OUR TAKE

Alex’s thoughts:

- The amount of the noise in Q2 2025 has surprised everyone, including us, once again. There is a lot of uncertainty on so many fronts at the same time: trade, immigration, fiscal policy, regulation, and defence.

- The great news - it is hard to imagine things getting worse from here. I believe that the peak damage to the economy will happen soon or already happened – and this is probably all that matters in the markets. Stock markets are forward looking - reflecting where the economy might be 1-2 years from now, i.e. time when the economy might already start to recover from the damage caused by uncertainty in global trade.

- The bad news is that markets have recovered too fast and too aggressively and potentially became vulnerable to eventual speed bumps in economic recovery in the next few 1-2 years. Therefore, it became much harder to find great companies at attractive prices for our portfolios, compared to just 3 months ago.

- While the likelihood of 10%+ correction in Canadian and U.S. markets has significantly increased, we are not expecting a correction larger than 20% in the near term, because central banks can lower interest rates further in both Canada and U.S., and U.S. has the option to soften it’s the trade policy, and U.S. economy might continue to benefit from aggressive investments in A.I. and infrastructure.

- U.S. exceptionalism has been tested before - while global investors are re-evaluating it again, we think the U.S. will continue to attract human and financial capital more than other regions of the world. The reason is that it is still the most investor friendly jurisdiction in the world, notwithstanding all the present chaos.

Chris’s thoughts:

- Picking up on Alex’s point regarding US exceptionalism, and the current chaos, I am reminded that within my lifetime, we have had similar periods of public mistrust and downright dire economic prospects for the USA. I recall the corruption and the skullduggery of Nixon years, I recall the early 70’s oil embargo and the long line ups just to fuel your vehicle. I recall the Japanese answer to our gas guzzlers and as the popularity of Toyota, Honda and Datsun cars displaced our North American brands. At that time, there was much speculation that Japan would become the world’s leading economic power. Not so many years ago, it was China that was to become the world’s dominant economic power. Maybe they will, but if they do it will be the first centrally planned economy with a severe aging demographic issue and lack of freedom to do so. My view, it is not going to happen. Yes, the U.S. has some issues and often those issues don’t get dealt with until the rest of the world forces you to deal with them. It happened in Canada during the Chretien/Paul Martin years, when the world told Canadians we have to cut government spending – and we did. Let’s remember, we are less than 18 months away from the US midterm elections and 30 months from the end of Trump 2.0. Five years from now, it will seem like a blip on the screen. As Buffett likes to opine, nobody ever made a plug nickel betting against the USA.

- Notwithstanding the above point, our heads are not in the sand. To protect ourselves against the current economic and political issues, mostly emanating from the U.S., we have more exposure to the gold complex than I have had in my entire career. We have reallocated $USD denominated investments to $CAD and other jurisdictions.

- What if we are wrong and the U.S. fails to maintain its “most business friendly” jurisdiction in the world? Let’s remember that the Roman empire did not fall in a day – nor did the Dutch, The Portuguese, The Spaniards, and the British. Please rest assured we are always on the lookout for alternatives. For example, we are becoming increasingly interested in the fast growing and business friendly United Arab Emirates. Alex, Eileen and I have a strongly vested interest in preserving and growing all the funds entrusted to our care.

THE PLAN

- Staying calm and rational amid today’s relentless noise. The survival instinct is forcing investors to scan for threats—and sensational headlines only amplify those fears. On top of that, investors are increasingly frustrated with government policy at home and abroad, which can tempt them to invest based on "what is wrong” instead of "what is.”

- Keeping the existing U.S. market exposure in The Dividend Value Discipline (TM) strategy. Despite increasing likelihood of a short-term correction, we think our diversified exposure to high quality names will serve us well in the long run. We have a positive bias to industrial, technology, basic materials, and energy sectors. We have a neutral bias U.S. dollar exposure.

- Keeping the existing Canadian market exposure in all our strategies, with a positive bias to the energy, utilities, and materials sectors. We have a strong positive bias to natural gas, uranium, and precious metals, and a neutral bias to oil.

- Keeping our recent small additions to global markets in The Dividend Value Discipline (TM) strategy – German and Chinese equities and potentially adding a bit of exposure to a third foreign market.

- Keeping the above average level of cash in old and new accounts, to exploit future opportunities.

- Continuing our relentless search for companies with great cultures, competitive advantage, and favourable industry tailwinds, at attractive prices.

TEAM UPDATE

Our team had another great quarter of processional growth and meaningful activities outside work.

Margo:

“I recently enrolled in the Canadian Securities Course (CSC), and I’m incredibly grateful for the opportunity to expand my knowledge and deepen my understanding of the industry. It’s exciting to be investing in my professional growth. Also, as a new addition to the team, I’ve really enjoyed getting to know both my colleagues and our clients. Every conversation helps me feel more connected and reinforces how much I value the relationships we’re building. It’s been a great start, and I’m excited to continue contributing to the team and supporting our clients’ goals.”

Sebastian – our new intern and CRM expert:

“I'm grateful to work with the Aspira team. The mentorship and support since May have helped me grow both professionally and personally. I've learned so much just being part of this group. I've really enjoyed being in the office. I learn something new every day, and it's inspiring to see how hard everyone works and the joy they find in helping others.”

Jasmin – our new marketing expert:

“I recently made a career switch at Raymond James - from Branch Administrator to Marketing Assistant for Aspira Wealth! I’m excited to start this new journey with a great team who has been supportive and helpful.

Also, I recently took a small road trip up to Squamish during my time off. I stopped at a few viewpoints and Shannon Falls on our way there and back. It was so fun and a wonderful way to spend a hot summer day.”

Maxim:

"Proud to start my 4th year at Aspira as an accredited CFA charterholder.

Recently, I’ve been reflecting on how the structure and discipline I apply in the gym and Muay Thai training mirror the principles of our investment research - both require consistency, resilience, and a long-term mindset.

I am also grateful for opportunities to recharge with weekend getaways around Moldova and Europe.”

Ben:

“I’m excited about the team we have in place at Aspira – in particular, Margo and I have been working really well together for the last few months, and I’m looking forward to our continued improved efficiency as a team.

I was in Kamloops recently to referee the youth soccer provincial championships – it was great to mentor some newer referees, and I had a blast being a part of one of the wonderful final with a national berth on the line.”

Eileen:

“I’m excited to share a personal milestone - I've recently earned my CRPC® (Chartered Retirement Planning Counselor) designation. This enhances my ability to support clients with cross-border financial planning.

And on a lighter note - two weekends ago, I had the pleasure of participating in the ALS Foundation’s annual charity golf tournament. While our team didn’t take home the trophy, we were proud to be the only all-female team in the field, which in our books made us number one!”

Alex:

“I am grateful to our clients for the trust in managing their hard-earned savings in an incredibly stressful year like 2025.

On the family front, I am happy that we survived a 130 km fundraiser bike ride with my 14-year-old daughter (thanks again for your donations!) and also excited with my middle daughter choosing to study science at UVic from September 2025, after successfully completing the Challenge program at Mt. Doug High School.

Chris:

“Excited to be celebrating his Mum’s 90th birthday this summer, we three generations in tow all the way to Pugwash, Nova Scotia.

Looking forward to hosting our next podcast, from Generation to Generation, with Sandy Pollack, author of Don’t Leave Mess! How to Disaster - Proof Your Family Legacy.”

Alex Vozian, CFA

Co-Founder and Portfolio Manager of Aspira Wealth

July 11, 2025.

The information contained in this report was obtained from sources believed to be reliable, however, we cannot represent that it is accurate or complete and it should not be considered personal tax advice. This report is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views expressed are those of the author and not necessarily those of Raymond James. We are not tax advisors, and we recommend that clients seek independent advice from a professional advisor on tax-related matters. This provides links to other Internet sites for the convenience of users. Raymond James Ltd./Raymond James (USA) Ltd is not responsible for the availability or content of these external sites, nor does Raymond James Ltd/Raymond James (USA) Ltd endorse, warrant or guarantee the products, services or information described or offered at these other Internet sites. Users cannot assume that the external sites will abide by the same Privacy Policy which Raymond James Ltd/Raymond James (USA) Ltd adheres to. Raymond James Ltd., Member—Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()